Ohio Energy Report: August 2025

Peak Loads for Summer 2025

Brakey Energy provides email and text alerts in advance of potential Capacity and Transmission Coincident Peaks (CPs) to those clients that elect to receive them. As of August 25, 2025, Brakey Energy has issued 14 Capacity CP alerts, 15 FE (ATSI Zone) Transmission CP alerts, and 4 AEP Ohio CP alerts during Summer 2025. Brakey Energy also issued 5 winter alerts for the AEP Zone in January of this year.

Capacity CPs occur during the five one-hour intervals when demand on the PJM grid is at its highest. Transmission CPs for FE customers occur during the five one-hour intervals when demand on FE’s zonal grid is at its highest. The Transmission CP for AEP customers occurs during the one-hour interval when demand on AEP’s zonal grid is at its highest.

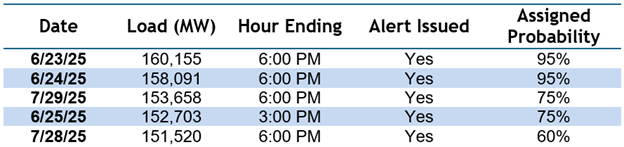

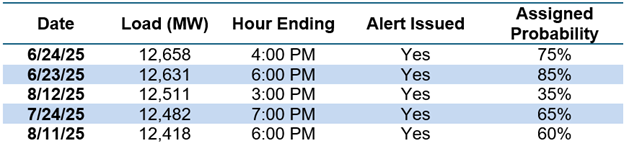

The tables below list PJM’s and FE’s five highest loads and AEP’s single highest load this year, as well as the day and time of each occurrence. This is based on preliminary data.

Table 1: Five Highest Loads for PJM through August 27, 2025

Table 2: Five Highest Loads for FE through August 27, 2025

Table 3: Single Highest Load for AEP through August 27, 2025

As we head into the month of September with cooler weather forecasts on the horizon, we believe there is a strong probability that many- if not all- of the PJM and ATSI loads listed in the tables above will be CPs come the end of the summer. Similarly, we maintain our belief that there is a strong likelihood that AEP’s load on January 22, 2025 will set the AEP Zone’s 1CP for the November 1, 2024, through October 31, 2025 CP year.

However, we know that forecasts can change quickly, and Brakey Energy will continue monitoring weather and load forecasts, issuing alerts to participating clients as warranted. If you are a Brakey Energy client and would like to receive these alerts, please contact Catherine Nickoson.

Ohio EDU Riders SGF and LGR Eliminated August 14

Earlier this month, all four of Ohio’s electric distribution utilities (EDU) – AEP Ohio, AES Ohio, Duke Energy, and FirstEnergy Ohio – filed updated tariffs for the Legacy Generation Resource Rider (Rider LGR) and the Solar Generation Fund Rider (Rider SGF). These revisions set both riders to zero for bills rendered on or after August 14, the date House Bill 15 (HB 15) took effect.

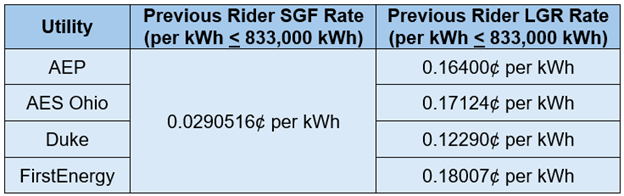

Signed by Governor Mike DeWine on May 15, 2025, HB 15 repealed Rider LGR and Rider SGF, which had been in place since January 1, 2020, following the passage of House Bill 6 (HB 6). Rider LGR collected costs associated with two coal-fired power plants in Cheshire, Ohio, and Madison, Indiana, owned by the Ohio Valley Electric Corporation (OVEC), in which AEP, AES Ohio, and Duke hold ownership stakes. Rider SGF, also created by HB 6, took effect January 1, 2021, and provided $20 million annually in out-of-market payments to qualifying solar generation facilities.

For non-residential customers, both riders were billed on a per-kilowatt-hour (kWh) basis for the first 833,000 kWh consumed during a billing period. Customers using at least 833,000 kWh per month will save $242 per month from the elimination of Rider SGF. Eliminating Rider LGR will produce slightly higher savings, which vary by utility. For example, a FirstEnergy non-residential customer using at least 833,000 kWh per month will see a $1,500 per month reduction in distribution charges, while a similar Duke customer will save about $1,024 per month.

Table 4 below shows Rider SGF and Rider LGR rates in effect prior to August 14.

Table 4: Previous Rider SGF and Rider LGR Rates by Ohio EDU

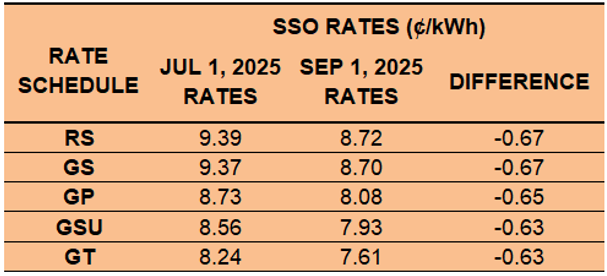

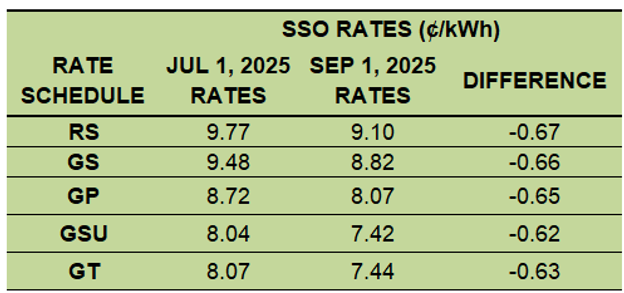

FirstEnergy’s SSO Rates Change September 1

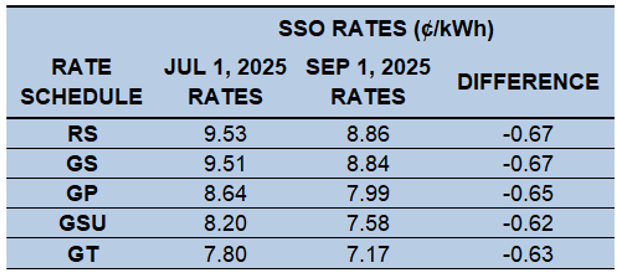

Electric costs will be decreasing slightly on September 1 for Ohio Edison (OE), The Illuminating Company (CEI), and Toledo Edison (TE) customers that take electric generation service under the utilities’ Standard Service Offer (SSO). The SSO is the default rate charged by the utility for generation services to customers that do not contract with an alternative supplier. The SSO generation rate is higher during the three summer months of June, July, and August than it is during the other nine months of the year.

The current and September 1, 2025 SSO rates per kilowatt hour (kWh) for customers served under OE, CEI, and TE Residential (RS), Secondary (GS), Primary (GP), Subtransmission (GSU), and Transmission (GT) rate schedules are shown in the tables below. These rates will change again on October 1, 2025.

Table 5: OE SSO Rates

Table 6: CEI SSO Rates

Table 7: TE SSO Rates

If you are not receiving electric generation service from an alternative supplier and would like more information about how FE’s SSO rate update will impact your monthly electric costs, please contact Katie Emling.

Residential Corner

The sky-high Base Residual Auction (BRA) clearing price has resulted in all offers being materially higher than what customers are accustomed to. Users looking to hide on a low short-term rate can contract with American Power & Gas for three months at a low 6.09¢ per kWh. Just know that this is a teaser rate and be sure to enter into a new contract before expiration to avoid a sky-high holdover provision!

For those who have been under American Power & Gas for a teaser rate in the last year, they probably will not let you sign up for that promotional offer. In that case, Major Energy is offering a similar three-month offer for 6.39¢ per kWh.

The best longer term option is a 8.29¢ 12-month offer from Energy Harbor. These types of high prices are going to be a shock to residential customers, but there is no getting around this surge in capacity prices.

Regarding natural gas, Brakey Energy has long and often found defaulting to distribution utilities’ SCO a prudent strategy for natural gas supply. We encourage our readers to utilize this strategy if they are comfortable riding the highly volatile natural gas market. To employ this strategy, you simply need to provide a termination notice to your existing supplier and you will automatically be defaulted to the SCO.

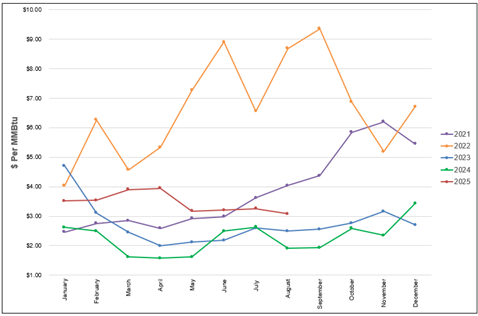

Natural Gas Market Update

The NYMEX price for August settled at $3.081 per Million British Thermal Units (MMBtu) on July 29, 2025. This price is down 5.5% from the July 2025 price of $3.261 per MMBtu. This settlement price is used to calculate August gas supply costs for customers that contract for a NYMEX-based index gas product.

The graph below shows the year-over-year monthly NYMEX settlement prices for 2021, 2022, 2023, 2024, and 2025 year-to-date. Prices shown are in dollars per MMBtu of natural gas.

Figure 1: NYMEX Monthly Natural Gas Settlement Prices

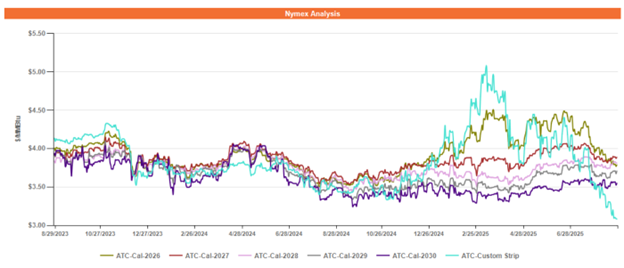

Figure 2 below shows the historical August 28, 2023 through August 28, 2025 Around the Clock (ATC) forward NYMEX natural gas prices in dollars per MMBtu for the balance of 2025 (labeled as “Custom Strip”) and calendar years 2026, 2027, 2028, 2029, and 2030.

Figure 2: ATC Calendar Year NYMEX Natural Gas Prices

*Pricing courtesy of Direct Energy Business.

Forward gas prices have softened overall since the beginning of the summer – particularly in the short term through May 2026 – largely due to record-high gas production, averaging 107.5 billion cubic-feet (BCF) per day in July. Furthermore, despite the heat this summer, power burn demand has trended lower compared to last summer, thanks to increased power generation from coal and solar.

Forward gas prices from June 2026 onwards remain in a state of backwardation, as fast-increasing global liquefied natural gas (LNG) export capacity could create a supply glut, depressing domestic natural gas prices.

Electricity Market Update

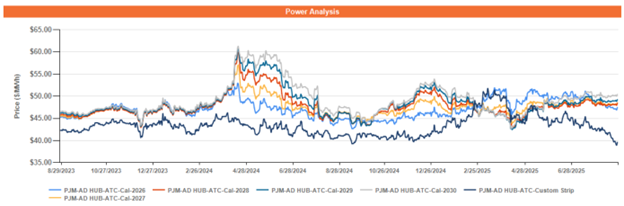

Figure 3 below shows the historical August 28, 2023 through August 28, 2025 ATC forward power prices in dollars per Megawatt hour (MWh) for the balance of 2025 (labeled as “Custom Strip”) and calendar years 2026, 2027, 2028, 2029, and 2030 for the AD Hub.

Figure 3: ATC Calendar Year Power Prices for the AD Hub

*Pricing courtesy of Direct Energy Business.

Having been in a state of backwardation since this past winter, forward power prices for calendar years 2026 through 2029 have recently coalesced and are all trading at approximately the same level. The results of the most recent capacity auction have sent the message to market participants that capacity prices will remain very high for the foreseeable future. All else equal, higher capacity prices have a depressant effect on forward power prices, as generators are able to recoup their costs with higher capacity payments rather than charging more for the energy component – the generation of the electron.

Forward power prices through mid-2026 have also followed trends in the forward natural gas market, though the softness has been less pronounced. Record-high gas production, healthy storage injections and levels, and the expectation of moderating weather to close out the summer have caused gas prices through May 2026 to soften markedly since the beginning of the summer.