Ohio Energy Report: June 2026

Inaugural Ohio Energy Leadership Summit Brings Ohio Energy Users Together in Cleveland

The inaugural Ohio Energy Leadership Summit (“Summit”) took place on Tuesday, June 16, at the Hilton Cleveland Downtown, bringing together approximately 140 commercial and industrial energy users, electric and gas distribution utility executives, legislators, and other energy professionals for a full day of discussion on Ohio’s evolving energy landscape.

Presented by the Ohio Energy Leadership Council (OELC) and co-sponsored by BakerHostetler and Dynegy, the Summit was designed as a practical forum for large energy users to hear directly from industry leaders on utility rates, reliability, infrastructure investment, and strategies for managing rising energy costs.

The day began with welcoming remarks from Renee Rambo of Johns Manville, a member of OELC’s Board of Directors, framing the Summit’s purpose: fostering collaborative dialogue among customers, utilities, and other stakeholders at a time of significant change in Ohio’s energy markets. The first panel focused on Ohio electric and gas utilities, centered on reliability, modernization, infrastructure investment, and how commercial and industrial customers may be affected by future utility spending.

Throughout the day, sessions addressed electric and natural gas rate trends, transmission and capacity costs, utility programs, and customer strategies for controlling costs. Brakey Energy team members including Matt Brakey, President and Katie Emling, Energy Analyst, presented in three of the Summit’s breakout sessions. The Summit also provided valuable networking time, connecting attendees with peers, service providers, and policymakers facing many of the same challenges.

On behalf of OELC, Brakey Energy would like to thank all those who attended and contributed to making this inaugural Summit a successful day of education, advocacy, and networking.

Figure 1. Ohio Electric and Gas Utility Panel Discussion at the Ohio Energy Leadership Summit.

Left to right: Matt McKenzie (AEP Ohio), Josh Davis (Enbridge Gas Ohio), Russ Lang (Ferroglobe), Renee Rambo (Johns Manville), David Proano (BakerHostetler), and Matt Brakey (Brakey Energy).

FirstEnergy Files Proposed Data Center Tariff

On June 12, 2026, Ohio Edison, The Cleveland Electric Illuminating Company, and The Toledo Edison Company filed an application with the Public Utilities Commission of Ohio seeking approval of a new Data Center Tariff, Schedule DCT. The filing follows a PUCO directive requiring the FirstEnergy (FE) utilities to create a separate class for data centers to help ensure that future costs are properly allocated to those customers and not shifted to other nonresidential and residential customers.

FE’s proposed tariff would apply to data center operators, including mobile data centers and cryptocurrency mining facilities. The tariff would require data center customers to take service under the normally applicable rate schedule for their service voltage, but with additional protections such as long-term contract requirements, collateral tied to the cost of new infrastructure, and a minimum monthly billing demand equal to the greater of actual usage or 85% of contract capacity. New data center load would also not be eligible to participate in FirstEnergy’s Non-Market Based Services Rider transmission pilot program.

The proposal is similar in concept to AEP Ohio Power Company’s (Ohio Power) Data Center Tariff, which went into effect in July 2025. Both address the same issue: data centers can create large infrastructure needs, and utilities want assurance that the data center customer, not other customers, will be responsible for costs if a project does not materialize or fails to use its reserved capacity.

However, there are important differences between FE’s proposed DCT and Ohio Power’s Schedule DCT. Ohio Power’s tariff is generally focused on large new or expanded data center loads of 25 MW or more, while FE’s proposal does not include a stated minimum load threshold. FE also proposes a minimum contract term generally equal to the load ramp period plus ten years, compared with Ohio Power’s load ramp period plus eight years. FE’s filing reflects a continued move by Ohio utilities toward specialized rate structures for data centers, balancing economic development against protections for existing customers.

Ohio Energy Costs Expected to Remain Elevated

A recent Crain’s Cleveland Business article published on June 15, 2026, warned that Ohio’s electricity costs have risen sharply and are likely to remain elevated or even continue rising in the years ahead. Retail electric prices for Ohio Edison customers in Northeast Ohio have essentially doubled over the last five years, while utilities and grid operators are planning billions of dollars in additional investments to maintain reliability and serve growing demand.

A major driver is the rapid growth of data centers, particularly newer AI facilities that require enormous amounts of power around the clock. Matt Brakey, President of Brakey Energy, explained that while earlier cryptocurrency-related loads were often flexible and could reduce usage during grid stress, many AI data centers are “24/7 operations” with far less ability to curtail. That lack of flexibility is placing upward pressure on costs even as the supply side faces its own challenges.

The changing generation mix is another key factor. As older coal-fired power plants have retired, replacement resources have not always provided the same dispatchable capability during periods of high demand. Brakey emphasized that the grid still needs resources that can operate when demand is highest, noting that wind and solar often fall short during peak demand hours because they are “not dispatchable.” This has grown more important as PJM’s capacity prices have risen sharply, reflecting a tighter supply and demand balance across the regional grid.

Adding new generation and transmission infrastructure will take time. Brakey noted that new dispatchable thermal generation can take years to come online, and that supply chain constraints are creating “multi-year backlogs” for critical equipment. In short, even with agreement that more supply is needed, building it may take years.

For commercial and industrial customers, the takeaway is clear: elevated energy costs are unlikely to be temporary. Customers that actively manage peak demand, evaluate procurement strategies, monitor utility rate cases and tariff changes, and participate in demand response or other cost-management opportunities will be better positioned to control costs.

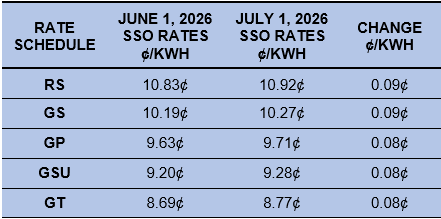

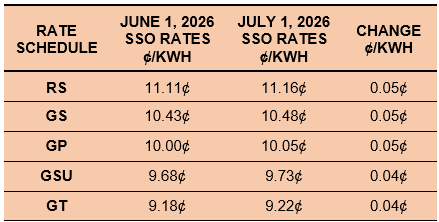

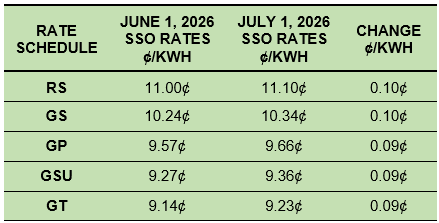

FirstEnergy Announces Updates to SSO Rates

Compared to one year ago, July 1 electric costs for FirstEnergy (FE) customers that take electric generation service under Ohio Edison’s (OE), the Illuminating Company’s (CEI), and Toledo Edison’s (TE) Standard Service Offer (SSO) will be approximately 1.15¢ per kWh higher on average across all FE companies and rate schedules. The SSO is the default rate charged by the utility for generation services to customers that do not contract with an alternative supplier. FE’s SSO generation rates are higher in the three summer months of June, July, and August than in the other nine months.

The tables below compare the current and July 1 SSO rates per kWh for OE, CEI, and TE Residential (RS), Secondary (GS), Primary (GP), Subtransmission (GSU), and Transmission (GT) rate schedules. These rates will change again on September 1.

Table 1: OE SSO Rates

Table 2: CEI SSO Rates

Table 3: TE SSO Rates

In our experience, these SSO rates include a healthy supplier risk premium compared to competitive market options. If you are a nonresidential customer nearing the end of your current electric generation agreement and do not wish to default to FE’s standard service offer, please contact Brandon Powers.

Residential Corner

Sky-high capacity prices coupled with increased data center demand have kept residential rates at the highest levels in recent memory. We recommend customers with an approaching contract expiration migrate to a 12-month offer with Better Buy Energy for 9.19¢/kWh.

Regarding natural gas, Brakey Energy has long viewed the distribution utilities’ Standard Choice Offer (SCO) as a prudent default strategy for supply. However, this approach can produce volatile bill outcomes, like the wild ride many customers experienced during the extreme cold earlier this winter. With natural gas settlement prices since remaining reasonable, customers on the SCO are likely seeing manageable bills.

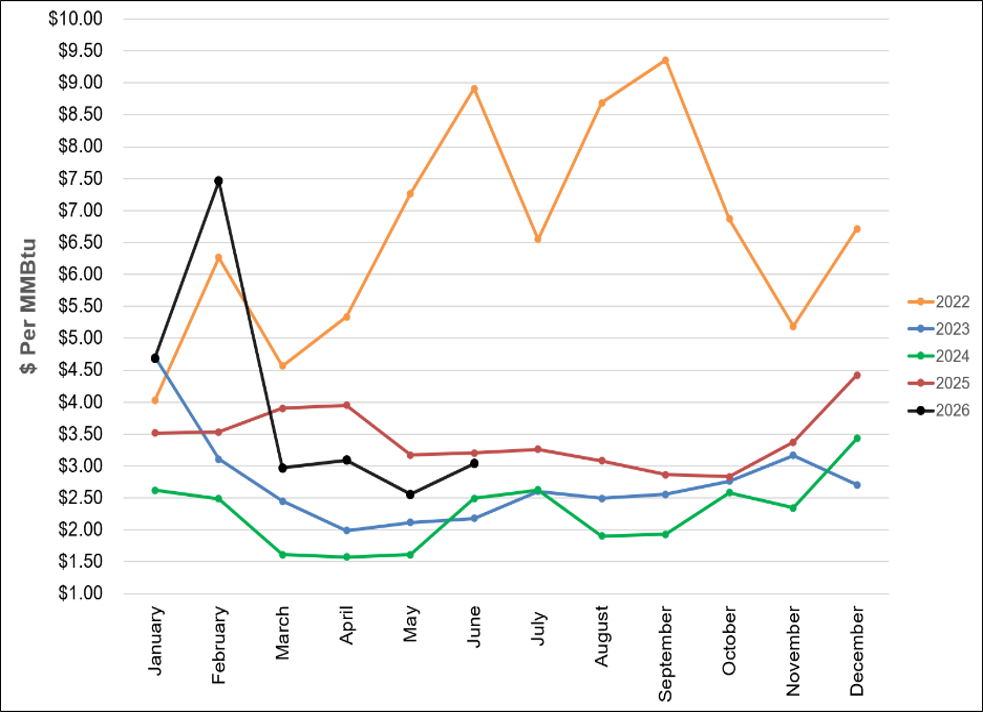

Natural Gas Market Update

The NYMEX price for June settled at $3.040 per Million British Thermal Units (MMBtu) on May 27, 2026. This price is up 18.8% from the May 2026 price of $2.559 per MMBtu. This settlement price is used to calculate June gas supply costs for customers that contract for a NYMEX-based index gas product.

The graph below shows the year-over-year monthly NYMEX settlement prices for 2022, 2023, 2024, 2025, and 2026 year to date. Prices shown are in dollars per MMBtu of natural gas.

Figure 2: NYMEX Monthly Natural Gas Settlement Prices

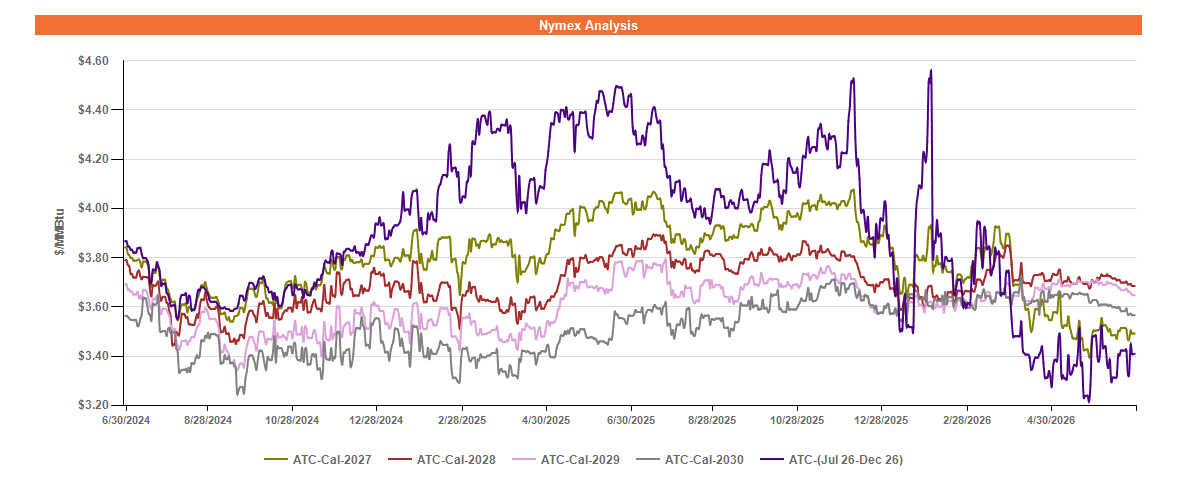

Figure 3 below shows the historical June 29, 2024 through June 29, 2026 Around the Clock (ATC) forward NYMEX natural gas prices in dollars per MMBtu for the balance of 2026 (labeled as “Custom Strip”) and calendar years 2027, 2028, 2029, and 2030.

Figure 3: ATC Calendar Year NYMEX Natural Gas Prices

*Pricing courtesy of Direct Energy Business.

Forward natural gas prices for the balance of 2026 have remained volatile but rangebound around their 2-year lows for the past two months. While trends in the oil market suggest the Iran Conflict is nearing resolution, forward gas prices for the balance of the year are likely to remain sensitive to any new developments, along with ever-changing summer weather forecasts.

For calendar year 2027 and beyond, forward gas prices have also traded lower over the past two months, but with less volatility than the balance of 2026. Domestic gas production has rebounded after a brief dip in late April and early May and now sits near record levels. Gas in storage sits at a slight surplus to the 5-year average, and the U.S. Energy Information Administration (EIA) projects healthy storage heading into winter. This has helped soften forward gas prices in all outlier years, especially 2027, now trading near 2-year lows.

Electricity Market Update

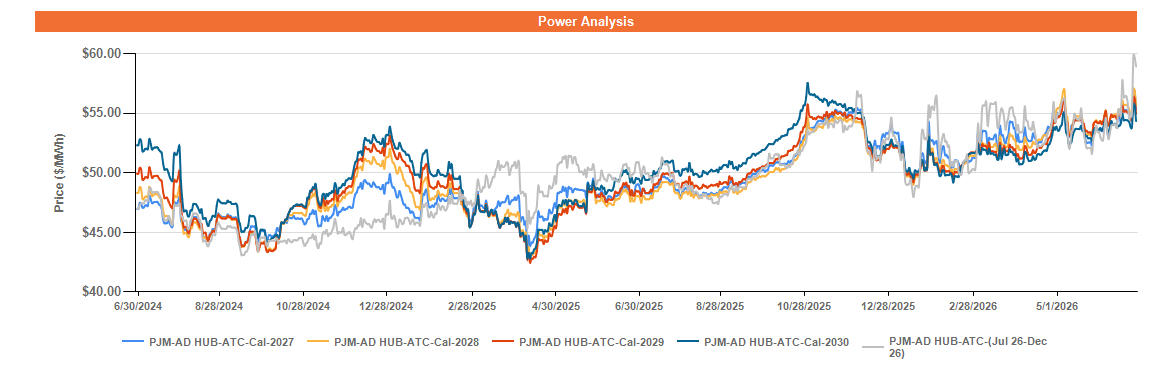

Figure 4 below shows the historical June 29, 2024 – June 29, 2026 ATC forward power prices in dollars per Megawatt hour (MWh) for the balance of 2026 (labeled as “Custom Strip”) and calendar years 2027, 2028, 2029, and 2030 for the AD Hub.

Figure 4: ATC Calendar Year Power Prices for the AD Hub

*Pricing courtesy of Direct Energy Business.

Forward power prices have continued to trade at or near multi-year highs, not only for the balance of 2026, but for outlier years as well, and in contrast to the forward gas market, which has trended lower since winter’s end.

As data center loads have begun materializing on the grid, rather than existing only as projected future demand, PJM’s supply-demand fundamentals have evolved. Although natural gas prices remain relatively low, growing electricity demand and tightening reserve margins have increased the likelihood that higher-cost generation resources will be needed to satisfy peak demand and maintain required operating reserves. This is contributing to higher locational marginal prices (“LMPs”) and, in turn, helping to keep forward power prices elevated.

Historically, efficient combined-cycle natural gas generators have frequently set the marginal price. Today, however, expectations of stronger load growth, tighter reserve margins, and greater reliance on higher-cost resources during peak conditions have reduced the degree to which forward power prices move in tandem with natural gas prices. These developments help to explain why forward power prices have remained near multi-year highs despite the recent softening in the forward natural gas market.